The world is a big place, but U.S. real estate has been a compelling investment for non-U.S. persons for a long time. There is a lot to consider when structuring this investment, though, and there is no “one-size-fits-all” approach. To determine which holding structure may provide the greatest advantages, non-U.S. investors must consider the types of income expected to be generated, anticipated plans for repatriating earnings, and potential exit from the investment, among other factors. Or, put another way, we want to begin with the end in mind. Below are some general considerations for non-U.S. investors, but to develop a plan specific to your needs, please reach out to one of our advisors, who can help you determine the appropriate structure for your investment.

Questions? Masataka Yamaguchi and Isaac Jones are here to help.

General U.S. Taxation Rules

Although non-U.S. persons are generally not subject to tax in the U.S., non-U.S. persons can be subject to U.S. federal income tax under certain circumstances, including, but not limited to, the following:

- Fixed, determinable, annual, or periodic income (FDAP). U.S. source FDAP payments made to non-U.S. tax residents are subject to U.S. withholding tax at a rate of 30% on a gross basis, unless reduced under an income tax treaty. Common examples of such payments include dividends paid by U.S. companies and interest paid by U.S. obligors.

- Income that is effectively connected with a U.S. trade or business (ECI). ECI derived by non-U.S. individuals is subject to U.S. tax on a net basis at graduated ordinary income tax rates of, under current law, up to 37%. ECI derived by non-U.S. corporations is subject to U.S. tax on a net basis at the current federal corporate income tax rate of 21%.

- Foreign Investment in Real Property Tax Act (FIRPTA). Where a non-U.S. person disposes of a U.S. real property interest, the FIRPTA provisions treat any gain on disposal as ECI, subject to the U.S. federal ordinary income tax rates outlined above. In addition, the FIRPTA provisions require the purchaser to withhold tax at a rate of 15% of the gross proceeds, unless an exemption applies. It should be noted that this withholding amount is a prepayment of the U.S. federal income tax due upon disposal, as opposed to an additional tax.

Given the various ways in which U.S. activities of non-U.S. investors may be taxed, careful structuring of an investment in U.S. real estate is very important.

Direct Investment in U.S. Real Estate

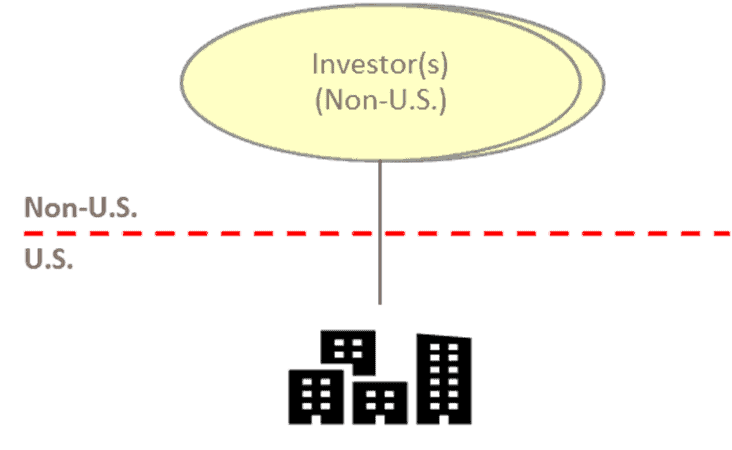

Perhaps the simplest structure is for a non-U.S. person to invest in U.S. real estate by acquiring and holding the U.S. real estate directly (or through an entity that is treated as transparent from a U.S. federal income tax perspective, such as a limited partnership or a single-member limited liability company). [See Fig. 1]. In such a structure, rental income received by the non-U.S. investor should be treated as FDAP and, as such, U.S. withholding tax at a rate of 30% would generally be imposed on the gross rental income. Where certain conditions are met, however, an election may be made to treat the rental income as ECI, allowing for deductions to be claimed against the gross income and for the net rental income to be subject to U.S. federal income tax at the ordinary income tax rates outlined above. Additionally, the non-U.S. person may be required to file a U.S. income tax return, which could be burdensome and create privacy concerns for certain non-U.S. investors.

If the U.S. real estate is held directly by a non-U.S. corporation, the non-U.S. corporation should also be subject to an annual U.S. branch profits tax (BPT). The BPT is imposed at a rate of 30% on the non-U.S. corporation’s “dividend equivalent amount,” which, very broadly, is determined by assessing the changes in the non-U.S. corporation’s U.S. net equity during the year. The BPT generally attempts to equalize an investment by a non-U.S. person through a branch with an investment through a U.S. corporation. As with the 30% withholding tax imposed on FDAP income, the BPT rate may also be reduced under an income tax treaty. When earnings generated by the U.S. real estate activities are repatriated, no second layer of U.S. taxation should occur with such a direct investment.

Upon disposal of the U.S. real estate by the non-U.S. investor, the FIRPTA provisions should treat any gain as ECI, subject to U.S. federal ordinary income tax rates. In addition, the purchaser should be required to withhold tax at a rate of 15% of the proceeds, unless an exemption applies.

Indirect Investment through a U.S. C Corporation

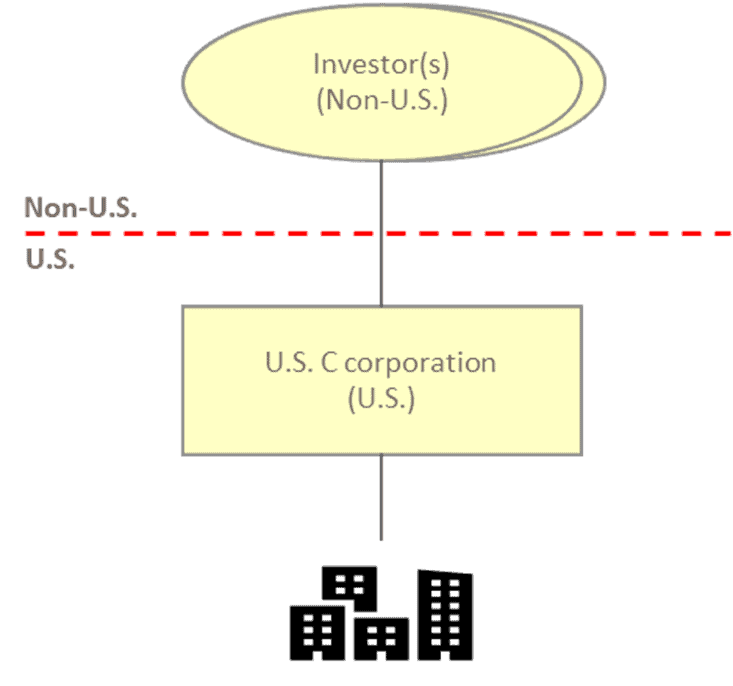

As an alternative structure, the non-U.S. investor could consider forming a U.S. C corporation that would hold the U.S. property. [See Fig. 2]. In such a structure, the U.S. corporation should be subject to U.S. federal income tax at a rate of 21% on the net income generated by the property. In contrast to the direct investment scenario, the non-U.S. shareholders should not be subject to U.S. tax on the ongoing income. Also, as the investment is being made through a U.S. corporation as opposed to through a U.S. branch, the BPT should not apply.

If earnings are repatriated from the U.S. corporation to the non-U.S. shareholders by way of a dividend, a 30% withholding tax should apply, unless reduced under an income tax treaty. For U.S. federal income tax purposes, however, a distribution is treated as a dividend only to the extent of the greater of the U.S. corporation’s current or accumulated earnings and profits (E&P). Any distribution in excess of E&P is treated as a return of capital (which is generally not subject to U.S. tax) and, subsequently, capital gain.

In the real estate context, the U.S. corporation’s E&P may be minimal due to interest and tax depreciation deductions and, accordingly, the U.S. corporation may be able to minimize the portion of the distribution treated as a dividend (and which is subject to withholding tax) and, instead, maximize the portion treated as a return of capital, depending upon the non-U.S. shareholder’s basis in the U.S. corporation.

While this structure does result in two levels of taxation (i.e., income is taxed at the level of the U.S. corporation and such earnings are taxed again at the level of the non-U.S. shareholders upon repatriation), it should be noted that, as with its E&P, the U.S. corporation’s taxable income may be reduced by interest and depreciation deductions, thereby reducing the effective tax rate.

Upon exit, gain from the sale of the U.S. real estate should be subject to U.S. tax at the level of the U.S. corporation at the current federal corporate income tax rate of 21%. Where certain conditions are met, the U.S. corporation could subsequently distribute the net proceeds to the non-U.S. shareholders in a liquidating distribution that should not incur a second layer of U.S. tax.

If, instead, the non-U.S. shareholders exit by selling shares in the U.S. corporation, the FIRPTA provisions should apply to treat the U.S. corporation as a U.S. real property interest, resulting in any gain being subject to U.S. tax at the level of the non-U.S. shareholders at ordinary income tax rates.

Indirect Investment through a Non-U.S. Corporation Blocker

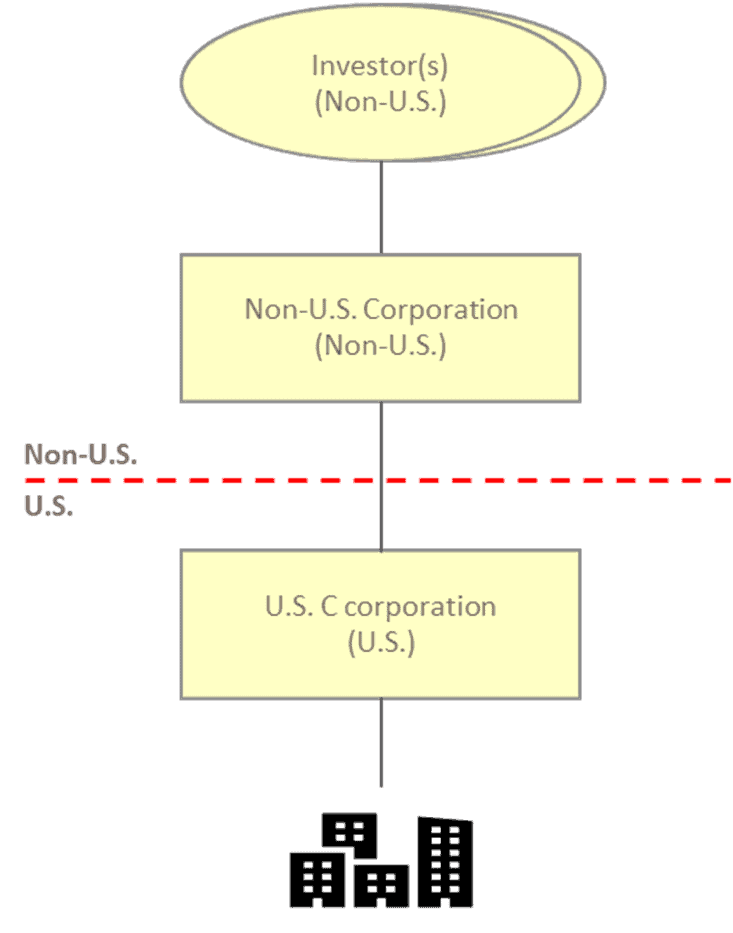

A third alternative that could be considered is for the non-U.S. investors to form a non-U.S. corporation that forms a U.S. C corporation to hold the property. [See Fig. 3]. The U.S. tax implications of such a structure are broadly similar to those set out above for ownership via a U.S. C corporation, with two important additional considerations. First, the use of a non-U.S. corporation as a non-U.S. situs asset may limit the potential exposure to U.S. estate tax – exposure that is generally present in the previous example. Second, such a structure provides the option for the non-U.S. shareholders to exit by way of a sale of shares in the non-U.S. corporation without any U.S tax. Of course, whether such an exit is feasible from a commercial standpoint would need to be assessed.

Other Considerations

Several additional factors can impact the total effective tax rate that should be considered when determining the optimal holding structure. Such considerations include whether the investment will be made via debt or equity (including an assessment of the relevant interest expense limitation rules), the amount of tax depreciation deductions that may be available, the applicable U.S. state and local taxes, eligibility for income tax treaty benefits, and, of course, the non-U.S. tax implications.

Disclaimer: The information contained in this communication, including attachments and enclosures, is not intended to be a complete analysis of all related issues. Nor is it sufficient to avoid tax-related penalties. It has been prepared for informational purposes and general guidance only and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is made as to the accuracy or completeness of the information contained in this publication, and Perkins & Company, its members, employees and agents accept no liability, and disclaim all responsibility, for the consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it.

Written by Sebastian Biddlecombe, Tiffany Ippolito, and David Hemmerling. Copyright © 2021 BDO USA, LLP. All rights reserved. www.bdo.com